What a US$3 million transaction that travelled half the world tells us about the global financial system

A new investigation details suspicious payments connected to a luxurious London mansion with a politically exposed resident. We take a close look at a Swiss bank involved in one of the key transactions.

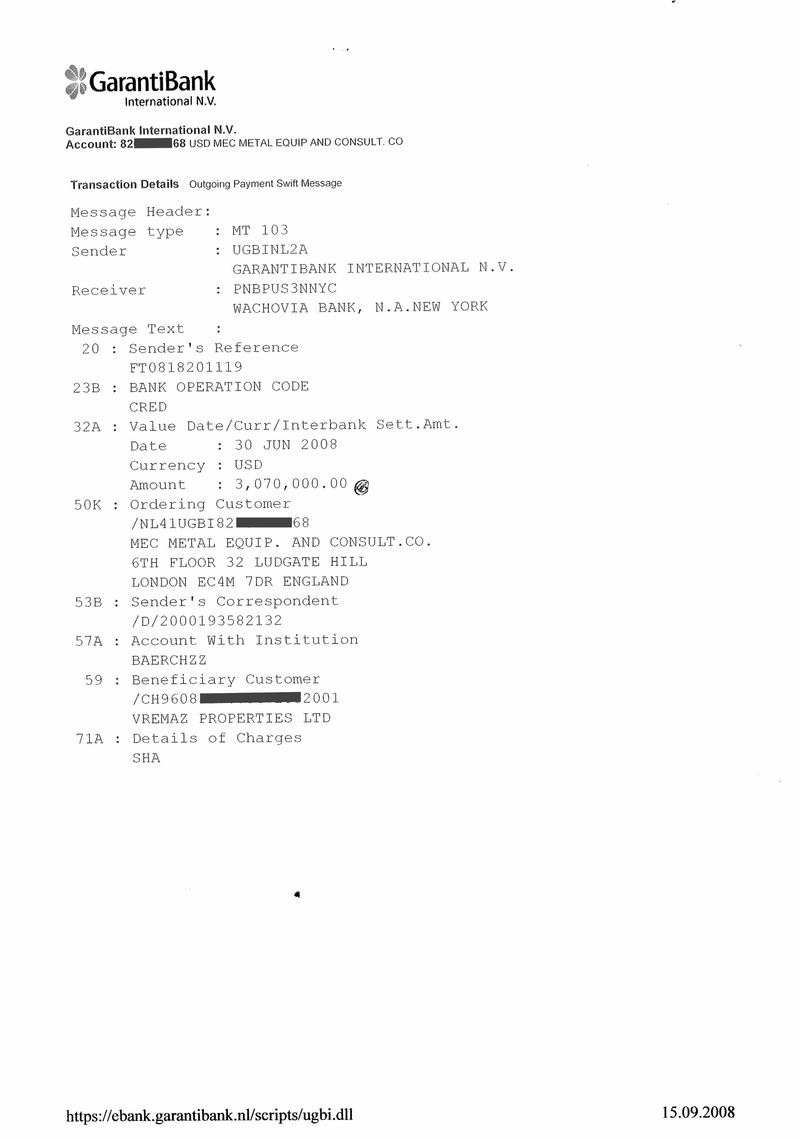

Image: Transparency International

A British limited liability company transfers US$3.07 million to the Swiss bank account of an offshore firm, Vremax Properties Limited, a company registered in the British Virgin Islands (BVI), for general consultancy services. A couple of months later, Vremax purchases a luxury property in London and gives permission to a 29-year-old from Azerbaijan to live there. In the following two years, Vremax purchases two next-door apartments and the adjacent corridor. The young Azerbaijani lodger, on behalf of the company, requests permission from the London council to renovate the apartments, transforming them in a single luxurious mansion.

Thanks to the Panama Papers, we know that the British company that transferred the funds to Vremax is connected to the Turkish construction magnate Mehmet Cengiz. But, besides the transfer, there is no information on his or his company’s relationship with Vremax.

He does, however, have a relationship with Azerbaijan, where he was awarded a contract by a state water resources management company managed by the father of the young Azerbaijani who now lives in the London mansion.

This is what a new investigation by the Organized Crime and Corruption Reporting Project (OCCRP) reveals.

In the absence of publicly available data on foreign property ownership in the UK and on beneficial ownership of companies in the BVI, more information – including on who de facto owns the property – can only be provided by:

- the responsible corporate service provider in the BVI,

- the UK solicitor involved in the property transaction, and

- the Swiss Bank where the company held an account.

This is assuming they all fulfilled their anti-money laundering obligation and identified the beneficial owner of their clients.

Red flags everywhere

If these professionals indeed fulfilled their anti-money laundering requirements of identifying and verifying the identity of the beneficial owner of companies and checking the sources of funds and wealth, it is likely these transactions should have raised questions and led to further investigations.

The case revealed by OCCRP shows many of the textbook examples of red flags potentially related to money laundering through real estate:

- Overseas ownership

- Transactions involving legal persons or arrangements domiciled in tax havens or risk territories

- Transactions involving legal entities with no actual business activity

- Transactions with funds from countries considered to be tax havens or risk territories.

- The source of the funds used to finance the real estate transaction was from abroad, in particular, from offshore jurisdictions or jurisdictions that have strict bank secrecy.

We cannot tell whether suspicions have been raised with authorities and if investigations have been carried out. But there are relevant hints that suggest that it should have and that authorities should look into the deal.

US$3 million – for what?

Suspicion should have arisen also when the US$3 million landed in Vremax account in June 2008. According to the OCCRP investigation, the metadata of the consultancy contract between Vremax and MEC Metal Equipment & Consultancy Co shows that the file appears to have been created three months after the transfer was made. This means the bank involved in this transaction may have received the payment without any evidence of what it referred to.

According to international anti-money laundering standards, banks should conduct due diligence checks for each customer – such as complete client identification – and confirm the nature and purpose of business. These steps should help banks draw a risk profile for each customer.

For customers considered as high-risk – such as politically exposed persons (PEPs), their family members and associates – the bank should take additional measures, like enhanced due diligence (checking the source of funds and wealth, for example) and senior management approval. In monitoring transactions, the bank should be satisfied that the transaction meets the client profile and that there is sufficient evidence that justifies it. If this is not the case, the bank should request more information and report suspicious activity, if not satisfied.

Weak anti-money laundering defences

The bank in question is Julius Baer, headquartered in Switzerland.

If confirmed that the funds could be connected to corruption and money laundering, it would not be the first time the bank finds itself embroiled in a controversy. The Swiss bank has also been the bank of choice of Venezuelans, other Latin American and FIFA officials allegedly involved in corruption scandals in recent years.

In October, the bank announced it is seeking to withhold bonuses from former CEOs over money-laundering scandals dating to their times leading the Swiss private bank.

The bank’s decision comes after the Swiss Financial Market Supervisory Authority (FINMA) found that Julius Baer fell significantly short in combating money laundering between 2009 and early 2018, including in connection to the FIFA and Venezuela scandals.

What the FINMA investigation reveals

Earlier this year, an investigation conducted by FINMA included the analysis of 70 business relationships on the basis of risk and more than 150 sample transactions that took place between 2008 and 2018. The investigation revealed multiple irregularities.

- Information collected as part of customer due diligence (CDD) was often incomplete. The bank did not do enough to determine the identities of clients, nor to understand the purpose or background of its business relationships or the source of wealth of customers.

- Transactions were not properly monitored or were insufficiently queried. The bank failed to request more information or flag suspicious transactions even in cases where there was sufficient and known evidence against the customers.

- Compliance and risk culture were poor. The bank continuously promoted a high-risk appetite among managers and client advisers by financially remunerating those who brought more funds to the bank, without taking into account money laundering and other financial crime considerations. Special bonuses reserved to “top performers” included client advisers who had several of their clients reported as suspicious in connection with corruption cases.

- Compliance department was disempowered. The bank’s compliance department did flag, on certain occasions, money laundering risks related to specific customers or transactions. However, quite often these were not properly acted on.

The investigations by FINMA also concluded that the identified failings were not confined to a single adviser – that is, they were not a case of a few ‘bad apples’ inside of the bank – but rather that it was a systemic problem.

In addition to the Venezuela and FIFA money laundering cases, which were analysed by FINMA, there is also evidence of Julius Baer’s alleged involvement in the Lava Jato scandal.

Given the extent of failings identified, could there be more? If the same types of failings apply to the case of the US$3-million-transaction mentioned in the new OCCRP story, for example, it can well be that the bank won’t be in a position to tell who the person benefitting from the funds is, nor explain the main purpose of the account held by the company.

This week, Julius Baer also announced it also reached an agreement with the U.S. Department of Justice (DOJ) to settle an investigation into its role in the FIFA corruption scandal.

The types of failings identified in the latest investigations against the bank raise serious questions about the adequacy of anti-money laundering checks carried out by the bank.

A worldwide problem

Banks, as gatekeepers of the financial sector, have the task to prevent and detect illicit funds entering the financial market.

The recent FinCEN Files investigations show that banks across the world, and especially those in key financial centres, have an unacceptably high tolerance of risks when it comes to money laundering, corruption and other financial crimes. More often than not, they accept high risk clients and process suspicious transactions without asking all the necessary questions and putting in place the adequate mitigation measures. The FinCEN Files show that many banks ended up submitting suspicious activity reports to authorities years after the actual transactions took place and only when the alleged involvement of their customer in corruption or money laundering had become public knowledge.

The FinCEN Files show only the tip of the iceberg that is the global financial system’s vulnerability to abuse by criminals and the corrupt.

Supervisory authorities, on the other hand, seem to be failing to ensure that the risk-appetite of financial institutions is aligned with the anti-money laundering defences they themselves have in place.

They should not be waiting for the next big scandal – as we saw with Danske Bank – to undertake a comprehensive assessment of banks’ anti-money laundering programmes. Assessments into whether banks adequately perform due diligence as well as collect and update all the necessary customer data. In addition, supervisory authorities should be checking whether or not the quantity and quality of the suspicious transaction reports submitted by banks align with their risk profile (types of customers and services provided, for example). This should not happen primarily as a result of specific investigations, but as part of regular exchanges between financial institutions and authorities.

Priorities

Advocacy

Countries

Regions

Projects

For any press inquiries please contact [email protected]

{kind=link}